PHOTOS: Nick Koutoufas

PHOTOS: Nick Koutoufas

This is the web version of a feature that originally appeared in Real Estate Forum magazine. To see the story in its original format, click here.

Following a year in which the commercial property investment market scaled new heights, 2016 may have seemed like a falling-off. In fact, it was one of the strongest years on on record, even if it was also a year buffeted by the headwinds of global, and domestic, uncertainties.

In 2017, that climate of uncertainty is likely to persist. The new administration’s policies appear to be giving the commercial real estate community some cause for concern as well as reasons for celebration. However, if anyone is prepared to realize opportunities amid the question marks, it’s the industry heavyweights who participated in the 12th Annual Capital Markets Symposium. Hosted by Real Estate Forum and Transwestern in December, the discussion covered topics ranging from conditions in markets and property sectors to what they see in store for this year.

STEVE PUMPER: The 10-year rate has risen since the election took place. What does that mean for your organizations on the acquisition, disposition or lending side?

STEVE PUMPER: The 10-year rate has risen since the election took place. What does that mean for your organizations on the acquisition, disposition or lending side?

PETER SIBILIA: Yes, there’s been an increase but if you compare it to January 2016, it wasn’t a big one. That doesn’t mean we’re not worried about it; the percentage increase is very high. So we’re watching the 10-year very closely as it relates to real estate pricing. Some of our research folks would say there’s really no correlation between cap rates and interest rates. That’s probably true over a very long term, but given where we are right now with rates and acquisition activity in general, continued increases throughout 2017 could have an impact.

In terms of opportunities, we’ve already seen some in that there aren’t a lot of takers in the marketplace right now, particularly on the domestic front. The challenge has been the wide gap between the pricing expectations of sellers and buyers. If there’s some meeting of the minds there, you could see a fairly productive 2017.

GARY RUFRANO: We haven’t seen a meaningful effect on pricing, either. It will eventually impact the the more highly levered secondary or tertiary place—there have been a number of retrades and the like, and for net-lease buyers, the increase has obviously had a huge impact on their overall returns. But for class A product, we haven’t seen much of a pricing discrepancy.

TUBA MALINOWSKI: In terms of acquisition and disposition activity, we don’t expect higher rates to meaningfully impact the Smart Markets Fund’s activity. As a core fund with minimal leverage, we underwrite with a focus on unlevered returns and conservatively use debt only to enhance returns. The highly levered buyer pool is more worried about it. The positive thing is that the supply pipeline is slowing down because it’s now more difficult to get construction financing, particularly for multifamily development. I’m actually more optimistic about multifamily than I was 12 months ago, when it looked like supply growth just wasn’t going to end.

DENNIS SCHUH: From a lending perspective, a rise in LIBOR is actually beneficial to our existing loan portfolio. Yet while I think an increase in rates is a healthy thing for the economy, we’re still at historically low rates and all-in borrowing costs. We are seeing a lot of interesting lending opportunities; we just need to sort of pass through this phase of uncertainty. While higher rates have been threatened for a long time, they’re actually a sign that the economy is on generally good footing.

DIMPESH DARJEE: Interest rates would have to rise by at least 100 to 200 basis points before we see any significant impact on valuations. There’s a whole generation of fund managers who are accustomed to low rates and may fear rising interest rates because they’re not accustomed to it. However, when interest rates rise, companies like ours are inherently more profitable, because it makes the tide rise as a whole. That, in general, will continue to spur investment, which will help the economy. So I think initially people may fear it, but will come to terms with it pretty quickly because of all of the other positive factors.

JOHN EHLI: Real estate returns can be strong whether it’s a low or high interest rate environment. In fact, some of the better returns have come at points in the cycle where we’ve had higher interest rates. If rates don’t move too quickly, then real estate investments can continue to perform well.

Rising rates can also help to temper new supply. Oversupply is the kryptonite to our ability to move rental rates and protect returns. If fundamentals remain strong to balanced, we will continue to see an active market for acquisitions, dispositions and financing.

MICHAEL DESIATO: Data from Real Capital Analytics show that US transaction volume declined 11% in 2016, partially thanks to a significant dropoff in portfolio and entity-level deals. To what do you attribute most of that decline?

PAUL BONEHAM: Part of it was that 2015 was a year of huge transactions—people that had big bets decided it’s time to hedge those bets and not be so dramatically exposed in a certain area. That ran its course. But 2016 was still a very normal, healthy year.

EHLI: If you think about where we were in January and February of 2016, the stock market was down and a big piece of the lending market—CMBS—had not yet re-emerged. Over the past few years a series of core funds and other real estate investments had performed very well, so there was some profit-taking to be had through the year. So we were coming off a number of very good years for most real estate investors, in terms of accomplishing their goals with investment and repositioning their portfolios. As such, investors were more disciplined and I think we see that reflected in the numbers.

SCHUH: We also had a very contentious election that captivated the world, let alone the country. The uncertainty behind that also slowed transactions.

MALINOWSKI: Fundamentals in most sectors are good, with some strong rent and occupancy growth. But in the first quarter of 2016, none of the acquisition officers nor portfolio managers, frankly, had the confidence to go after the larger acquisitions. The big issue is the spread between what sellers want for assets—the “whisper price”—and what buyers are willing to pay. Uncertainty about capital flows and the economy always creates some stagnation while pricing adjusts. I do anticipate an increase in portfolio activity, especially for industrial, as investors see fundamentals remain strong.

RUFRANO: I’ve seen more rebound calls on transactions being bid on. You’ll put a number out there, and if the seller didn’t agree, we’d almost always walk away. Now, we feel like we need to register a number at which we’d be happy to own that product. And more often than not we’re getting calls back asking us to tweak it. We try to be disciplined in the number we put out so that we maintain our credibility. If they call back in six weeks with a counter, we might underwrite it. But

EHLI: There’s a born-on date. Pricing is perishable.

RUFRANO: Exactly.

DESIATO: When you look at your investment activity in 2016 and your targeted goal for 2017, is it more or less aggressive?

SIBILIA: We’ll probably close out 2016 with half the volume we did in 2015. Domestic pension plans are going to be back in the market in 2017, though it’s going to be fairly contingent upon pricing. We’ll do about the same, maybe a little more, investment in 2017. We did about 40 transactions, a mix of core and value-add. If the capital markets cooperate, we may ramp up our plans.

SCHUH: We’re seeing a lot of really interesting lending opportunities for the mortgage REIT at Starwood, and even some interesting special situations in the equity space. We just raised $460 million of equity overnight; we target larger loans in primary markets and are definitely seeing opportunities for growth.

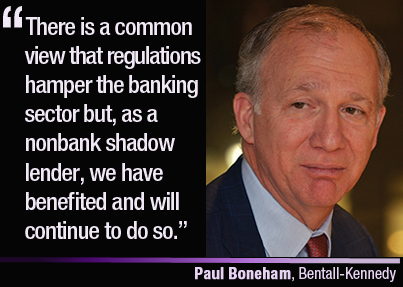

Increased financial regulations have certainly benefited those of us who are non-bank lenders. With the banks being clearly more conservative than they once were, we try to fill those voids in the market.

BONEHAM: Indeed, the regulatory climate has helped in terms of our lending activity. There’s a common view that regulations hamper the banking sector but, as a nonbank shadow lender, we’ve certainly benefited and will continue to do so. Virtual real estate portfolios on banks’ balance sheets have risen dramatically post-crisis; it’s one of the few areas where you’ve seen a tremendous amount of growth. There may be an opportunity to do some more deals of that nature before banking regulations get loosened.

If you look at our assets under management, we had a very strong year in terms of growth, but it came from a variety of sources. All in all, two things at play—how much capital you have coming your way and what the capital markets will supply in terms of acceptable product. Our transaction commitment for 2016 was very similar to 2015, and I think our projections for ’17 are in the same range, about $1.5 billion to $1.7 billion.

DARJEE: The debt space in general is an area in which everyone appears to be looking to grow, including us. Coming out of the downturn we went from a $1-billion to $2-billion program to one that exceeds $5 billion last year and the plan is to exceed that in 2017. I’m hearing similar things from our peers. There continues to be a great relative value and significant demand and so we’ll continue to grow as we raise new capital and expand into additional debt programs. And those numbers are just in the US. The global figure will be even larger, as we placed over $1 billion in Europe and grow our debt platform worldwide.

On the equity side, 2015 was spectacular and we were fortunate to acquire a number of large, high-quality transactions. We acquired about $7 billion nationally, which was one of the top years for TIAA. We’ve done about as many transactions in 2016, although we focused on some smaller deals and, dollar-wise, it was closer to $4 billion. If we get to a similar number in 2017, we’ll be happy. But there’s nothing saying we have to get there—we’re focused on quality deals.

EHLI: Our platform has capacity for new investment. We continue to see strong domestic and cross-border capital inflows and capital sources appear ample to match last year’s productivity in terms of acquisition activity. We continue to remain disciplined to add the right product to match our portfolio and investors’ needs.

BONEHAM: There’s a big difference between an open-end fund and a separate account, in terms of cash balance. Cash is a great performance indicator for an open-end fund but it brings a completely different level of pressure; you can’t sit on too much cash for too long. However, a separate account client will typically have a more disciplined approach—they’re more patient, they’re looking for just the right investment at their set price point. There’s a push and pull there.

MALINOWSKI: For us, transaction volume in 2016 was better than 2015, accounting for about $1.2 billion compared to $800 million. In 2017, unless we see some really great opportunities for our separate account clients, we should be back to that $800-million volume. The capital flows for core funds have slowed down and that has historically been a big driver of our acquisitions volume.

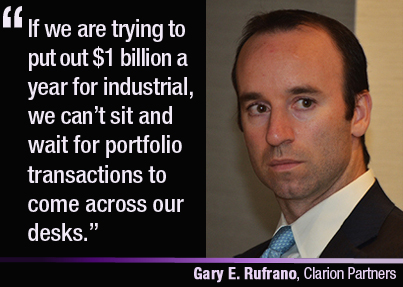

RUFRANO: We’re on track to earn about $4 billion in 2016. It’s hard to predict exactly what you’re going to do and when you’re going to find transactions. You don’t always match up with expectations, but we have available capital to do $4 billion-plus in 2017. It’s a tough market right now. For instance, we’ve had a queue in our industrial fund for some time. We staffed up in asset management and operations staff and felt we had to go into the market, so we bought $14-, $17-, $25-million industrial deals and rolled them up into our fund. The problem is, there’s so much demand for industrial product right now that we’ve held onto all the capital we have allocated for the sector.

SCHUH: We have a tough time making sense of smaller loans in our portfolio lending business. The whole-dollar profit on those small loans isn’t enough to make it worth your time or resources.

RUFRANO: That’s why we buy in the markets in which we already own product. Half the time spent on evaluating a new acquisition prospect is trying to understand how it plays in the market. It takes a lot more time than you want to think, because you’re not getting the appropriate reports. We’ve had to employ this strategy for some time. We do want to buy portfolios, but we just can’t count on them. If we’re trying to put out $1 billion a year for industrial, we can’t sit and wait for portfolio transactions to come across our desks.

PUMPER: What role is development playing within your investment strategies?

RUFRANO: We always endeavor to build a lot of industrial. We generally build between eight million and 10 million square feet of industrial a year. On the multifamily end, we own Gables Residential. We’ll continue to build there, but very selectively. Site selection is key; we’d rather not build at all than build on the wrong site. We will selectively build in certain suburbs that are highly populated, have immediate access to transportation and offer a discount to a CBD within a commutable distance. I don’t see us doing office development and we’d rather redevelop retail than build new.

BONEHAM: We’ve done a lot of development. I’d say about 50% of our capital committed over the past three years has gone toward ground-up development or significant repositioning of assets. We like both those approaches for multifamily and office. Our industrial portfolio is very strong, at 97% leased, and development there is strictly tied to available opportunities.

SIBILIA: Our feeling is that if you can execute your business plan and generate value within two years, you do it. Outside of that, we’re probably not taking on much risk. They say no one dies of old age, right? But the older you get, the more likely you are to have health problems. We don’t know where we are in the cycle, but the longer it goes on, the more likely it is to be impacted by an outside force. So if we can put off risk by two, three years, get out of a deal or even refinance, we can tackle that. But to be tied up in a four- to five-year development process? We’re probably not going to do that.

DARJEE: On the equity side, it’s not a major part of our program in the US. The investments in our general account run along a barbell, with very high-quality core product on one end and some development on the other end as a complement to generate higher yields. In London, however, development plays an important part as we’re a high-profile, best-in-class developer. As we grow our platform, we may grow into more of it in the US but I don’t expect development to be a major component of what we do in the immediate future.

PUMPER: How about the debt side? Has the general lack of construction financing presented any opportunities?

DARJEE: We aren’t really funding much in terms of construction. TIAA was known for its construction-perm financing, especially in the apartment space. We got out of that just prior to the downturn and have not gotten back in and don’t expect to do so. We do some ground-up construction financing through our bank program, although not a significant amount.

In terms of opportunities in that space, I’m not expecting anything significant. There’s been a moderate pullback in construction financing, but the expiration of the 421-a tax abatement has provided more of an impact. There was a lot of construction in the past few years and it’s slowed down some, but that allows properties to lease up, and I expect that will create upward pressure on rents again soon. As the new supply is absorbed, it will fuel construction again.

SCHUH: We’re trying to be opportunistic in trying to fill voids in the construction lending market. The banks have pulled back prematurely, and that’s presented a lot of opportunities. We’re doing loans that banks would have done 18 to 24 months ago. But we’re being highly selective and we sort of have the pick of the litter right now. Generally, we’re looking for deals where we can get our money deployed very quickly, such as redevelopment opportunities.

DESIATO: We’ve come to the final question that we pose every year, and we have a lot of factors to take into consideration today. What keeps you up at night, and what drives you forward?

EHLI: The nice thing about working on a core fund is that we’re very well balanced, with a low LTV ratio, good occupancy and strong rental growth. The market can be frightening because fundamentals have been good for so long, which usually means there might be something around the corner, but the fund is very well positioned for those types of things.

On a macro note, it boils down to one thing: the unknown. When asked this question a year ago my answer was that the thought of Donald Trump becoming president seemed like such a wild card and totally out of left field. But it happened. So the changeover in the executive branch is definitely going to trickle down to the other branches and agencies in the government. It’s going to impact the judiciary, the Department of Labor, the Department of Justice, tax and immigration laws—there’s going to be a lot of change in Washington, DC and I don’t think any of us, at this point, really know how that’s going to play out. But, by and large, we feel pretty good about the fundamentals in the leasing market outside of the Beltway. If supply continues to remain balanced, we expect another good year in 2017.

MALINOWSKI: I tend to agree with John that fundamentals are great. I manage an infinite life core fund so we don’t have to sell—that’s good. So from a real estate-specific standpoint, I’m not staying up at night worrying. The global issues are what worry me. Having grown up overseas, the protectionist rhetoric that’s taken over in so many different countries is bothersome. And with a new administration in DC, we’re trying to predict the unpredictable, right?

There are certainly some risks we may have worried about six months ago that a pro-business environment is going to alleviate—easing regulations will help the capital markets and fundraising, for instance. Healthcare is a resilient industry and whatever is done there is not going to change the fact that our population is aging. There may be some opportunities for private sector investment in infrastructure, but again, we don’t know yet. So there will be positives for business, which is good. But on the other side of that—free trade is good, and it’s good for ports and warehousing. Restrictions there may negatively impact the industrial sector, and changes in immigration laws will not be positive for the tech industry.

RUFRANO: Indeed, we hope that at least financial markets will strengthen. If anything, enhanced profitability by banks may have them expanding in certain markets like Midtown Manhattan. Turning to real estate, there’s not a lot we need to be concerned about in terms of our existing portfolio. From an acquisitions perspective, the challenge is coming up with assumptions as you’re forecasting. We’re long-term investors, generally 10-plus years. Sitting around a table with your investment committee and having eight people try to figure out what’s going to happen in the next four years is impossible. So we’re relying on long-term fundamentals, buying the right assets in the right locations.

A lot of markets are overpriced. If you talk to the firms out there that are collecting bids, there are more and more people at the top of the bell curve. But then there’s one person that’s way out there on the pricing spectrum, and they’re the ones winning the bid process. I’m waiting for that one person to fall away. At that point, pricing will return to more realistic levels. For a lot of the transactions you lose, you kind of scratch your head and want to know how someone underwrote it and managed to get an acceptable return.

BONEHAM: Our portfolio is as solid as I’ve seen it in a long time. So, the fundamentals of real estate are not concerning. I think the biggest single wild card is cybersecurity.

SCHUH: I echo a lot of those sentiments. One thing to point out is that higher interest rates’ potential impact on the housing market should definitely concern us. Housing is what took us into a deep global crisis. The housing market is a little shaky right now and there’s a fair amount of inventory in many parts of the country. Housing is very sensitive to rates and if something happens there, it could again have a broader impact.

SIBILIA: Being a part of J.P. Morgan, we’ve been very fortunate to have a lot of global reach and a lot of geopolitical analysis and the like. For the past 12 months, I’ve spent a lot of time listening in on global calls as it relates to Europe. Putting Brexit aside, there are three or four major elections coming up in Europe over the next 18 months that are going to shape the political landscape for that continent. I don’t know the outcomes, so there’s a lot of global risk. And combined with some of what’s coming out of the US in terms of policies, all of that is making many people in Europe and elsewhere nervous. When you have a situation with an unknown outcome, it’s very hard to look ahead and make predictions.

DARJEE: A lot of people mentioned the proposed policies. I think restricting free trade and immigration could pose some problems, especially in terms of labor issues. Steve Jobs once suggested that anyone educated in the US should receive a Green Card stapled to the back of their degrees. It’s important to keep the most educated people we have to continue to lead and fuel innovation; otherwise, we’re going to have a challenge finding enough people to fill certain fields.

In terms of infrastructure improvement, that’s something both sides of the aisle agree is sorely needed. For taxes, it depends on the approach. For instance, a reduction of corporate taxes may keep more money in the country and perhaps keep companies from relocating, which is good for jobs. But in general, I’m not a believer in trickle down economics. I’m not convinced it’s worked in the past.

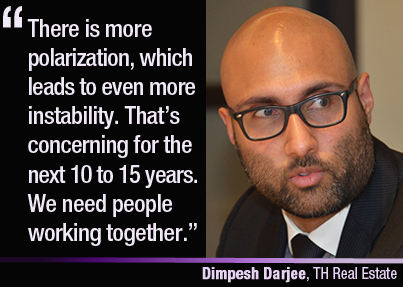

What does scare me is this: If you look at where our country is now, let alone many parts of the world, an increasing number of people live in communities that are very much like them. That doesn’t create a middle ground where you can engage in healthy debate. When people cluster around similarities, it leads to insulation and extreme thinking, because people want to differentiate themselves from the pack. In the extreme scenario it can lead to a revolution—I don’t see that here although we’re seeing the beginning of it in in other parts of the world.

In this country, we have a fair amount of segregation, be it Wall Street versus Main Street or the haves and have nots. There’s more polarization here and globally, which leads to more instability. That’s concerning because we’re in a totally different age—just look at the impact of the Internet. The tools available to us allow for much more extremity than in the past. That causes concern over where we might be in five, 10, 15 years. We need people working together, and unfortunately we’re seeing that less and less across the world.

What drives me forward is that in my lifetime I want to see advances in society pulling more countries and people around the world out of poverty and into the developed world. It’s the humane thing to do, and will ultimately help all of us and lead to a more stable world. I see it happening. The innovations during my lifetime give me confidence it can be done, but we have to want to do it.