NEW YORK CITY–Transaction activity across most property types dropped in January and February this year, falling to $61.4 billion, the lowest level in five years according to PwC's Insights Q1 report. Most property types were affected, with the exception of industrial, which posted a 40% increase in volume for the same period one year earlier — and after 2017 saw a 22% increase in volume compared to 2016.

![]()

PwC says one reason for the downward trend is that anticipation of increasing interest rates has further widened a gap between the bid and ask of buyers and sellers. “This is particularly evident in major metros where 2017 volume was down more than 15%, while volume in non-major metros increased nominally.”

However, PwC also noted that the pace of the decline has slowed as year-to-date volume fell less than 1% compared to the prior year.

That said, the overall tone of PwC's report was positive for the industry. Real estate operating fundamentals, pricing and deal activity remained stable in the first quarter it said. PwC attributes this stability to “the amount of capital available and the emergence of new market participants both domestically and internationally.”

“We are in the midst of a unique real estate environment that has us optimistic on the deals environment moving forward.”

Here are PwC's findings on the market's overall fundamentals.

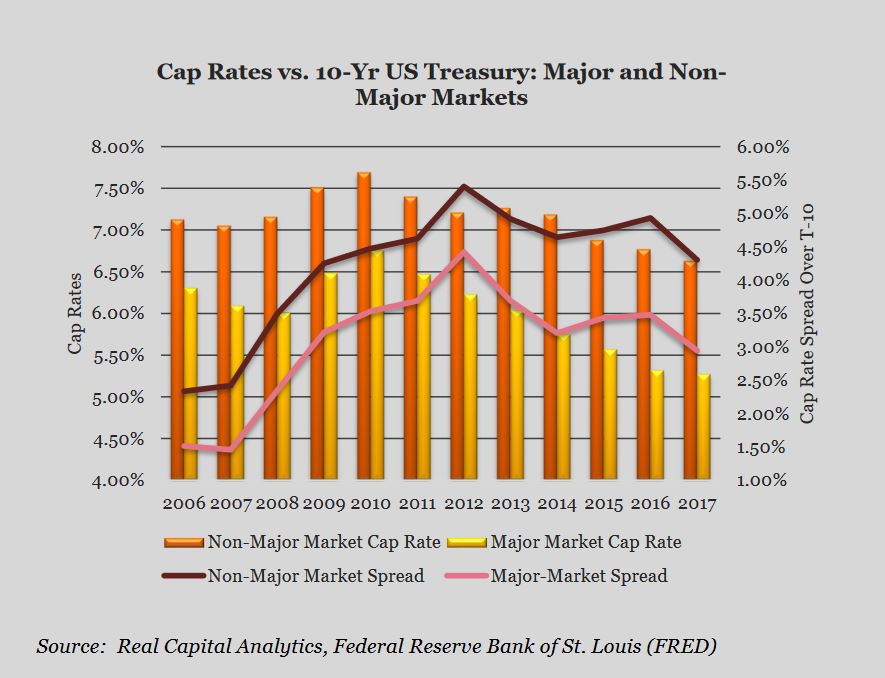

Cap Rates

As of year-end 2017, cap rates for major metros declined 5 basis points year over year and 13 basis points for non-major metros. PwC notes that the premium of cap rates relative to the 10-year US Treasury is well above prior cycle peaks. “Given the abundance of capital available and desire for yield, it is likely that pricing and cap rates will not see substantial movement in the near term.”

Multifamily Debt

With multifamily pricing remaining steady, investors are taking advantage of the plentiful debt available ahead of anticipated interest rate increases. Some $174.9 billion of capital flowed into multifamily debt during Q4 2017 and the total amount of outstanding debt is $46 billion more than any previous quarter and nearly $25 billion more than transaction volume, according to Federal Reserve figures. Refinancing activity is high, not surprisingly, and PwC notes that of the $27.4 billion of capital Freddie Mac provided during Q4 2017, 46% was designated for refinancings.

Foreign Investment

Foreign participation in the US CRE markets remain significant even as some players are stepping back. Middle East capital has all but ground to a halt, while capital flows from Asia have see annual declines of 7% since the peak in 2015, PwC reports. However, Singapore investors increased volume 189% to $9.5 billion in 2017 — an amount that was exceeded by Canadian investors, which accounted for more than one-third of overall activity.

Dry Powder

Globally, there was $266 billion available for investment as of March 2018 — a close to 7% increase over the $251 billion of dry powder available at year end, PwC reports. Valuation remains a concern for real estate fund managers; however their appetite for CRE does not show signs of subsiding, PwC said. CRE activity by sovereign wealth funds during Q1 2018 accounted for 45% of total expenditures, according to Sovereign Investors Institute figures.

© Touchpoint Markets, All Rights Reserved. Request academic re-use from www.copyright.com. All other uses, submit a request to [email protected]. For more inforrmation visit Asset & Logo Licensing.

Erika Morphy

Erika Morphy has been writing about commercial real estate at GlobeSt.com for more than ten years, covering the capital markets, the Mid-Atlantic region and national topics. She's a nerd so favorite examples of the former include accounting standards, Basel III and what Congress is brewing.