Another CRE Category Disrupted By M&A

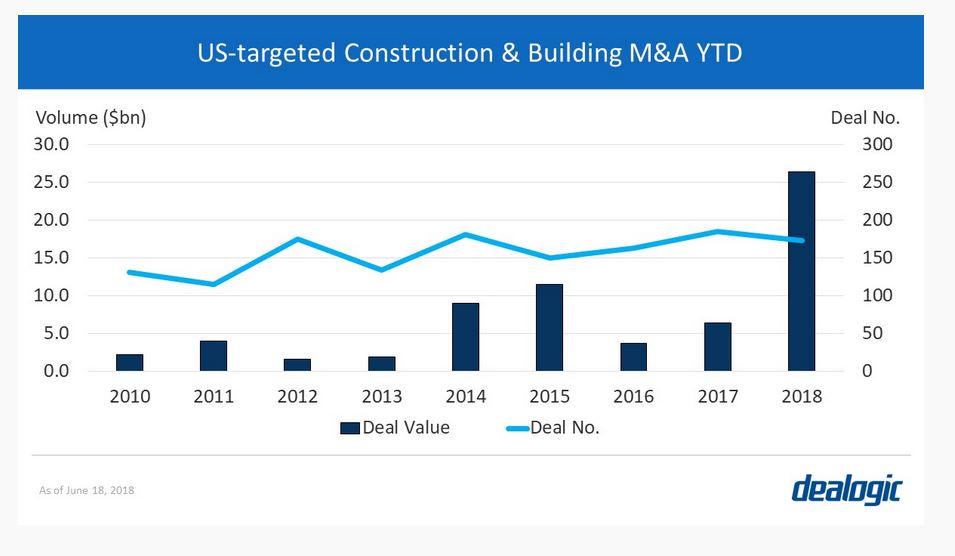

As of mid-June US-targeted construction & building M&A reached its highest year to date volume on record with 173 deals totaling $26.4 billion -- an increase of 312% compared to the same period last year, according to Dealogic.

LONDON–Mergers and acquisitions are in rapid-fire growth mode this year, not only in the US commercial real estate sector but across all sectors globally. GlobeSt.com has covered the numerous deals in our space but it is worth noting the activity outside of our realm for a few reasons.

So far this year there have been $2.35 trillion of deals announced, a 57% increase from the same period in 2017, according to Dealogic figures reported by The Wall Street Journal — 25 of which valued at $10 billion or more. Some recent examples cited by the Journal include Disney’s $71.3 billion agreement to purchase 21st Century Fox’s entertainment assets, Cigna Corp. agreement to buy Express Scripts Holding Co. for $54 billion and CVS Health $70 billion acquisition of Aetna.

Indirectly this activity will affect commercial real estate for better or worse as offices close due to consolidation and others open as new business units form and new markets beckon.

US Construction M&A At Record Levels

In a blog post Dealogic notes that US construction mergers and acquisitions are also rising to new heights.

As of mid-June US-targeted construction & building M&A reached its highest year to date volume on record with 173 deals totaling $26.4 billion — an increase of 312% compared to volume last YTD when $6.4 billion in US construction M&A closed via 183 deals.

{kind=link}

The drivers behind these deals included the federal government’s push for a massive increase in infrastructure spending, tax reform, which has increased investment in the industry and the possibility of new infrastructure projects on the horizon, according to Dealogic.

It writes:

As firms use strategic acquisitions to expand into new markets, volume for such deals reached their new record thanks to the announcement of several large deals—including the acquisitions of USG ($6.9bn), Westinghouse Electric ($4.6bn), and SRS Distribution ($3.0bn).

{kind=link}

Dealogic’s analysis ends on a sobering note though. It predicts that there could be a drop in the sector’s M&A volume in the near term.

The reasons include:

California’s new mandate requiring all new homes to have solar panels, increasing the overall cost for homebuilders. Interest rates have also been on the rise leading to higher mortgage rates for home buyers. With higher costs expected for both homebuilders and home buyers, the construction industry may see a decline in demand and M&A activity.