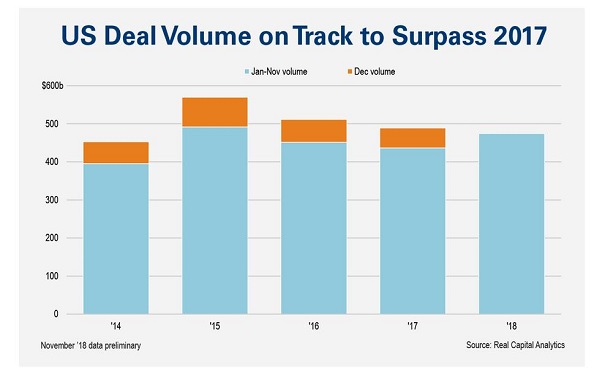

CRE Deal Volume On Track To Surpass 2017

“It would take a catastrophic December for the 2018 total not to surpass 2017 levels.”

{kind=link}

Investment sales for the last few months of 2018 — normally the most active period of the year — have admittedly been meh. But Real Capital Analytics says deal volume for 2018 is on track to exceed 2017’s.

Preliminary volume figures for November suggest a slowdown of investment activity, Real Capital Analytics noted in a recent post, with the slowdown in the fourth quarter more pronounced in the single asset market. The sale of individual assets fell at double-digit rates in October and November on a year-over-year basis, preliminary data shows, it wrote.

Meanwhile portfolio and entity-level transactions have become important drivers of deal activity both for November and the year overall. Preliminary figures for November suggest a 26% year-over-year pace of growth in such megadeals. On top of the 40% pace of growth in these deals in October, the fourth quarter may see an overall lift in deal volume largely because of megadeals, Real Capital Analytics writes.

Among the major five property types the office sector stands out as the only one posting declining deal activity for the year-to-date. Both the retail and industrial sectors are more than 20% ahead of the deal volume posted through November 2017; the hotel sector, meanwhile, is more than 40% ahead.

“With year-to-date 2018 deal volume already ahead of the level set through November 2017, it would take a catastrophic December for the 2018 total not to surpass 2017 levels,” it concludes.

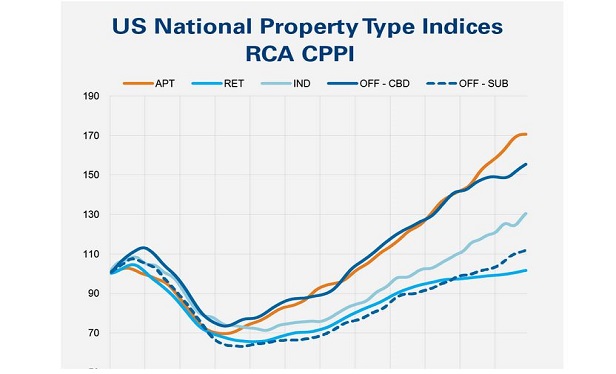

Separately, RCA also reports that US commercial property prices rose 7% in November from a year earlier, “logging a steady pace of increase consistent with the sustained investment sales growth in 2018 so far.”

The US National All-Property Index rose 0.6% from a month prior, the latest RCA CPPI report shows.

Annual price growth for industrial, CBD office and retail properties has accelerated for at least the past three months.

The multifamily asset class posted the fastest rate of growth for the quarter. Apartments saw prices rise 9% year-over-year, which was slower rate of increase than posted in the first half of 2018. Suburban offices posted the strongest acceleration in price growth so far this year; at the start of 2018 they were increasing at a 4.6% year-over-year pace, RCA writes.

{kind=link}